Cost allocation is a critical concept in accounting. It is a broad term, applying to several activities and methods.

Finance professional and managers use numerous techniques and methods to allocate business costs. Methods of cost allocation include the activity based costing method (ABC), time-driven activity based costing (TDABC), rate-based activity based costing (rate-based ABC), overhead cost allocation, reciprocal allocations, and the step-down method.

In this article, we outline some of these methods of cost allocation. While some techniques are logically distinct from each other, some can overlap. For instance, it may be logical to employ reciprocal allocations within overhead cost calculation, all within the umbrella of Time-Driven Activity Based Costing.

We begin with foundational concepts such as activity based costing, and move to discussing its time-based and rate-based variants. We then provide an overview of other concepts including direct and indirect costing, the step-down method. Finally, we outline reciprocal allocations. We use practical examples where possible to outline each concept.

Activity Based Costing (ABC)

A core concept in costing and accounting, ABC was first popularized in the 1980s. Activity based costing is an approach of identifying, and assigning costs within an organization, according to the activities that drive the costs, including overheads and indirect costs. ABC largely underlies the other cost allocation methods we outline here.

For example, imagine a furniture manufacturing company has three assembly line stages in its wooden furniture manufacturing process:

- Cutting Wood

- Assembly

- Prime & Paint

A picnic table might require 20 pieces of straight cut wood. Additional components may also be used to assemble. A dining table may require fewer pieces than a picnic table, but a higher number of distinct actions at the cutting station. The furniture company has concluded that all its cutting actions require roughly the same amount of time and resources. As a result, the company uses these actions as the basis for its “cutting station” allocations. Similarly, they measure assembly hourly. While they measure painting by volume used.

To complete the exercise in activity based costing, we could map the costs to these activities accordingly:

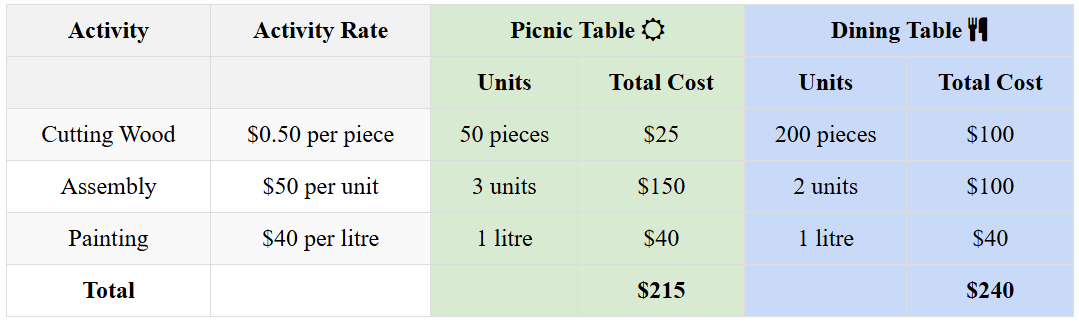

Picnic table:

- Cutting Wood (50 actions)

- Assembly (3 hours)

- Painting (2 litres)

Dining Table

- Cutting Wood (200 actions)

- Assembly (2 hours)

- Painting (1 litre)

For each of these activities, we must understand our unit cost and assign a value to each of the activities. This value will be consistent across all products. For example, the furniture company values wood cutting at $.50 per action, assembly at $50 per hour and painting at $40 per litre. Each of these costs may contain, for example, the labor costs, costs of running machinery associated with the given activity. Or they may contain and a share of fixed factory overheads. With these values in place, the furniture company can calculate the assembly line costs of their products according to their formula:

For a picnic table: Cutting of wood (50 x $0.50 per piece), Assembly (3 x $50), Painting (1 x $40), for a total cost of $215.

While for the dining table: Cutting of wood (200 x $0.50 per piece), Assembly (2 x $50), Painting (1 x $40), for a total cost of $240.

Cost Allocation outlined through an Activity Based Costing (ABC) cost calculation example

We include all costs related to the factory, assembly line machinery and labor costs in the above. In this instance, we would opt to calculate raw material costs for wood on a direct cost basis outside the activity based costing calculation. Adding these costs will give a total cost for the product along the ABC method of cost allocation. Click to read more examples of cost allocation and ABC from sports to wholesale retail.

Time-Driven Activity Based Costing

Time-driven activity-based costing builds on the above concept of ABC. With the time-driven activity based costing method, we cost each activity in terms of an hourly rate. This is instead of relying on time variable metrics like number of actions or quantities. Continuing with our previous example, the furniture company can calculate the costs of two new products as follows:

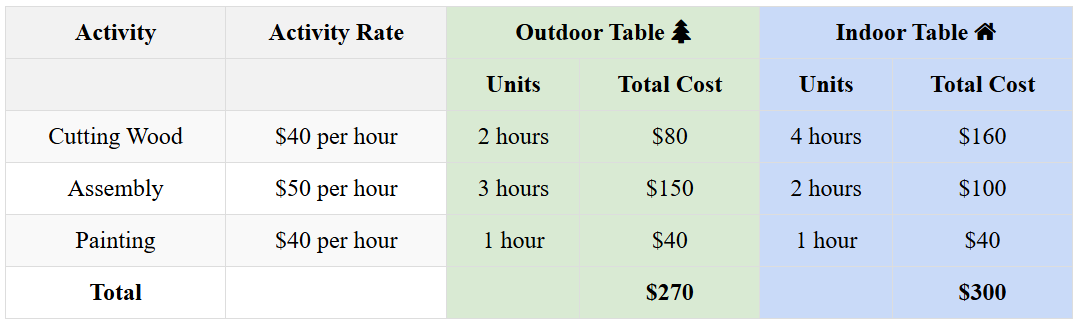

Outdoor table:

- Cutting Wood (2 hours)

- Assembly (3 hours)

- Painting (1 hour)

Indoor Table:

- Cutting Wood (4 hours)

- Assembly (2 hours)

- Painting (1 hour)

For the outdoor table: Cutting of wood (2 hours x $40 per hour), Assembly (3 x $50), Painting (1 x $40), for a total cost of $270

While for the indoor table: Cutting of wood (4 hours x $40 per hour), Assembly (2 x $50), Painting (1 x $40), for a total cost of $300.

Cost allocation outlined through a Time-Driven Activity Based Costing (TDABC) cost calculation example

Within each activity, we would calculate the various costs associated with the activity on an hourly basis. Two hours at the wood cutting station could include the costs of running machinery, labor costs for staffs, and the share of fixed overheads for the factory.

The company calculates its hourly rate for wood cutting to include:

- Labor Costs: Assuming an average of 2.5 FTE to run the wood cutting station, the factory can calculate the labor value based on its known labor inputs

- Machinery Costs: From energy to run the machinery to depreciation and maintenance, the factory can assign costs for machinery related to wood, divided by the number of productive hours.

- Overhead Costs: The factory can assign a share of overhead costs such as keeping the light and heat on in the factory, as well as indirect staff costs such as HR or the CEO here.

The hourly rate for each activity listed above can be dynamic. An unexpected rise in energy costs may see a modest increase to both the machinery and overhead categories. If the factory uses a cost allocation formula or software, they can adjust the inputs, and this will reflect in the calculation across all products. Read more for a complete guide on TDABC in your organization.

Rate-based Activity Based Costing (Rate-based ABC) vs Traditional ABC

Rate-based activity based costing is a simplified variation of traditional activity based costing. Use of Rate-based ABC streamlines the process by using a pre-defined rate for each calculation, rather than the detailed calculation of costs that is required from traditional ABC.

In traditional ABC, we emphasize extensive data collection, to ensure that our unit cost, hourly cost of a machine, or cost per action is highly accurate. In our example, it means that the furniture company would focus on understanding a cost per hour, or unit cost, to a high level of granularity.

Rate-based ABC allows us to rely on a generalized cost driver, in line with our example from earlier, we may denote $100 per hour as the assembly rate, rather than reaching a detailed estimate accurate to the cent. Using rate-based ABC may lead to less granularity in cost assignments, but allows for a faster implementation. Organizations who want to gain understanding from activity based costing, but do not wish to manage the overhead associated with managing the detailed calculations of traditional ABC, may benefit from Rate-Based ABC.

Direct and Indirect Methods of Cost Allocation

When allocating costs, it’s important to distinguish between direct vs indirect cost allocation methods.

Direct Costs

Direct costs are expenses that are directly tied to a specific cost object, such as a product, department, or project. For example, the raw materials (wood) we use in the manufacture of a picnic table. While direct costing is a straightforward costing method, it also has a role to play as a component of more complex cost models.

Indirect Costs

Indirect costs, on the other hand, are the expenses that we cannot directly trace to a single product or cost object, for example, the costs for energy, administrative staff salary, or factory overheads. These Indirect costs include all shared expenses, whether they are related to operations, production, or other activities.

Read a practical example of Direct vs Indirect costs for a US government agency with FEMA’s short breakdown of it’s indirect and direct costs.

Push & Pull Cost Allocation Methods

Push and pull allocations refer to distinct approaches that can be applied to many cost allocation methods. The approaches differ by whether costs are pushed through the system or pulled by specific products.

Push Allocations: In this cost allocation method, costs are “pushed” down from a central pool (such as a centralized IT department or the management office) to specific cost centers or products. We use the pull method to distribute indirect costs such as rent, utilities, or administrative expenses.

We can allocate the cost of office rent to different departments based on the square footage occupied by each. Alternatively, a pushed cost allocation driver for a finance department may be “expected number of invoices processed”, or a HR department may measure “average number of new employment contracts processed”. In push allocation, we aim to allocate exactly 100% of the overhead amount to cost drivers.

For example, in our furniture company, they would allocate the rate according to the expected hours used per product

Pull Allocations: Pull allocations use actual or expected output (or resource consumption data) to allocate costs. In this method, costs are “pulled” by specific products or services, from the resources or activities that provide the productivity needed.

If a furniture manufacturing company expanded to multiple plants of varying size, they could choose to allocate administrative labor overhead to each plant, based on the number of products produced by each site. This would be an example of using pull allocations to allocate their labor costs.

Pull allocations are particularly useful when the cost structure is volume-driven, meaning that costs are influenced by the level of activity. Organizations that are seeking accurate profitability analysis use this method. They may be looking to get a good grasp of the differences between actual costs and expected cost based upon volumes. The key distinction with pull allocations is costing based on the actual measured rates of activity, rather than expectations or averages.

As an example, a furniture company expects that each picnic table requires 3 hours of total production time, but the actual measured usage was 2 hours 44 minutes per table, then the actual figure will be used to apply ABC.

Step-down Method of Cost Allocation

Step-down costing is a method of allocating indirect (overhead) costs in organizations with multiple service and production departments. This method allocates costs from service departments to other departments (both overhead and productive), in a sequential order. This method ensures that all shared overhead costs are distributed, although it does not fully account for mutual services between service departments (which we discuss that next with reciprocal costing).

In our furniture company example, management will move through overheads sequentially to allocate their overhead to the correct department. Assume there are two production facilities; one manufactures chairs, and another tables. They are supported by three service departments. Ranking service departments is a prerequisite for step-down costing. For the furniture company, every department consumes IT costs, but it is managed without full-time staff or machine maintenance. Therefore, IT is logically ranked first in the allocation order. The ranking continues as follows:

- IT Costs: Every section of the business avails of IT services from the IT department. The IT department is not directly staffed, and includes hardware and licenses.

- HR Department: All staffed departments further down the chain incur HR related service costs, because they are each staffed by dedicated team members

- Maintenance Team: The maintenance team consumes IT and HR resources, but does not provide a service to them. It provides a service to both production departments. Therefore, it comes third in the ranking.

In this scenario, we first begin with the annual IT Costs ($50,000). They are allocated to the:

- HR Department (overhead) (20%) = $50,000 × 0.2 = $10,000

- Maintenance Team (overhead) (40%) = $50,000 × 0.4 = $20,000

- Production Facility A- Chairs (30%) = $50,000 × 0.3 = $15,000

- Production Facility B- Tables (10%) = $50,000 × 0.1 = $5,000

The HR budget ($60,000) can then be allocated to any departments further down the chain. In this instance we follow an equal apportionment basis where every staff member (FTE) accounts for the same amount of overhead.

- Maintenance Team (2 FTE) = $60,000 × 0.2 = $12,000

- Production Facility A- Chairs (6 FTE) = $60,000 × 0.6 = $36,000

- Production Facility B- Tables (2 FTE) = $60,000 × 0.2 = $12,000

Finally, we will allocate the budget for the shared maintenance team ($150,000) amongst the remaining departments. In this allocation, we will use a TDABC allocation, and allocate the costs based on the annual hours of maintenance staff consumed:

- Production Facility A- Chairs (1500 hours) = $150,000 × 0.6 = $90,000

- Production Facility B- Tables (1000 hours) = $150,000 × 0.4 = $60,000

Please note, in step-down costing, we rank the departments in logical order of whose services most impact another’s. We can only allocate costs further down the chain. In the event that we need to allocate a cost up the chain as well, we start with reciprocal allocations.

Reciprocal Method of Allocating Costs

Reciprocal services refer to situations when two or more departments provide services to each other. For example, in the above example, what if IT department was fully staffed and required HR allocation? IT provides support to the HR department, and the HR department provides human resource support back to the IT department.

Reciprocal allocation is the costing method used in these scenarios where interdepartmental services exist. Each department allocates costs to other departments and receives costs in return. This is a comprehensive cost allocation method. To perform a reciprocal allocation, the same ranking as the step-down method can be performed. However, in order to accurately allocate the overheads, simultaneous equations are performed. As complexity increases, organizations rely on accurate software and formulae to ensure the allocation of reciprocal costs.

Reciprocal allocations add some complexity by incorporating algebraic equations, but we consider them a critical method for accurate cost allocation in many organizations.

Summarizing: Methods of Cost Allocation

As you can see from this article, there are numerous methods and techniques that can be employed in cost allocation. From a rapid deployment of Rate-Based ABC to gain a broad overview, to detailed cost model covering dozens of activities, cost drivers and departments engineered using Reciprocal Allocations.

At enterprise-level, a robust system is a must. A purchased off-the-shelf solution like CostPerform, or one of its competitors, will generate a significant amount of value for most organizations operating at scale. The software is engineered to with the above methods accurately and with flexibility.

Click to read more by downloading our corporate allocations whitepaper, or contact us directly to request more information from our team. We have a large collection of resources available for those learning about cost allocation, whether just beginning or at a more advanced level. Click here to reach out to CostPerform or download the CostPerform Brochure now.